What happens to your retirement account when you file for bankruptcy?

When filing for bankruptcy in the Dallas area, whether under Chapter 7 or Chapter 13, it is crucial to understand how retirement accounts are treated, as this can significantly impact your financial planning and future security. Bankruptcy laws provide certain protections for retirement accounts to ensure that individuals have resources available for their retirement years, despite undergoing financial distress.

When filing for bankruptcy in the Dallas area, whether under Chapter 7 or Chapter 13, it is crucial to understand how retirement accounts are treated, as this can significantly impact your financial planning and future security. Bankruptcy laws provide certain protections for retirement accounts to ensure that individuals have resources available for their retirement years, despite undergoing financial distress.

Chapter 7 bankruptcy and retirement accounts

In a Chapter 7 bankruptcy, also known as liquidation bankruptcy, a debtor’s assets are sold off to pay creditors. However, most retirement accounts are exempt from this process, since they are safeguarded by federal bankruptcy laws. This means that 401(k)s, 403(b)s, profit-sharing, and IRAs (both Roth and traditional) are protected up to a certain amount. The exemption for IRAs is indexed for inflation and offers significant protection for individuals’ retirement savings. (more…)

For many Americans, debt is a way of life. When that debt continues to pile up, many people think that

For many Americans, debt is a way of life. When that debt continues to pile up, many people think that  With foreclosures in the Dallas area on the rise, we are hearing more and more questions about the rights that homeowners have during the foreclosure process. Foreclosure is obviously a challenging and confusing time, and understanding your rights is crucial for navigating the process effectively. Since we know more people are searching for these answers, I wanted to outline the key rights you have as a homeowner in Texas during foreclosure.

With foreclosures in the Dallas area on the rise, we are hearing more and more questions about the rights that homeowners have during the foreclosure process. Foreclosure is obviously a challenging and confusing time, and understanding your rights is crucial for navigating the process effectively. Since we know more people are searching for these answers, I wanted to outline the key rights you have as a homeowner in Texas during foreclosure. Only 51% of Americans in a recent survey were confident that they could pay off their credit card bills this month – a big increase from the same time period last year. Every month, LendingTree conducts its Credit Card Confidence Index, and the

Only 51% of Americans in a recent survey were confident that they could pay off their credit card bills this month – a big increase from the same time period last year. Every month, LendingTree conducts its Credit Card Confidence Index, and the  If you’re struggling with overwhelming debt and considering bankruptcy, the biggest question in your mind is probably “Which bankruptcy lawyer should I go to?” It’s one of the most important decisions to make – filing bankruptcy will have a significant impact on your life. Bankruptcy law is very complex, with many twists and turns, and traps for the unwary. If you need to file bankruptcy, choosing the right lawyer is critical.

If you’re struggling with overwhelming debt and considering bankruptcy, the biggest question in your mind is probably “Which bankruptcy lawyer should I go to?” It’s one of the most important decisions to make – filing bankruptcy will have a significant impact on your life. Bankruptcy law is very complex, with many twists and turns, and traps for the unwary. If you need to file bankruptcy, choosing the right lawyer is critical. Bankruptcy is more common than most people realize… In today’s world, it’s far too easy to accumulate overwhelming debt and lose control. While an unexpected bump in the road (like an automobile accident or loss of a job) can lead to a bankruptcy situation, many times, people start down the road to

Bankruptcy is more common than most people realize… In today’s world, it’s far too easy to accumulate overwhelming debt and lose control. While an unexpected bump in the road (like an automobile accident or loss of a job) can lead to a bankruptcy situation, many times, people start down the road to  Whether we are in a recession or not, it is not easy to earn enough to live comfortably in today’s world. You would be surprised to learn how many Dallas-area residents struggle on a monthly basis to simply make ends meed. Adding children or additional vehicle payments to the mix make a difficult situation even tougher. All it takes is one unexpected expense to send finances (and debt) spinning out of control.

Whether we are in a recession or not, it is not easy to earn enough to live comfortably in today’s world. You would be surprised to learn how many Dallas-area residents struggle on a monthly basis to simply make ends meed. Adding children or additional vehicle payments to the mix make a difficult situation even tougher. All it takes is one unexpected expense to send finances (and debt) spinning out of control.

When potential clients call us, they are usually stressed and scared. When you are drowning in uncontrollable debt, and you’re in danger of losing your car or your house, being afraid is understandable.

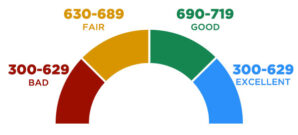

When potential clients call us, they are usually stressed and scared. When you are drowning in uncontrollable debt, and you’re in danger of losing your car or your house, being afraid is understandable. Everyone knows that their credit score is important – but most Americans don’t understand how the scores are assessed or affected by their actions. Ideally, you want a credit score in the 700-800 range, but what does that really mean – and how do you get there?

Everyone knows that their credit score is important – but most Americans don’t understand how the scores are assessed or affected by their actions. Ideally, you want a credit score in the 700-800 range, but what does that really mean – and how do you get there?