New York man dodges eviction for 20 years by abusing the bankruptcy system

One of the most common reasons that people file for bankruptcy is to stop foreclosure actions. Rubin & Associates help DFW area residents and property owners with cases like these quite often.

One of the most common reasons that people file for bankruptcy is to stop foreclosure actions. Rubin & Associates help DFW area residents and property owners with cases like these quite often.

Every once in a while, stories pop up about people who abuse the system, and one of the most extreme cases we have ever heard hit the news last month. Reported in major publications like Fox News and the New York Post, a man in New York has avoided eviction for more than 20 years by filing multiple bankruptcy cases.

According to the article at the New York Post, the man bought a Long Island home for $290,000 in 1998 and made his first mortgage payment to his lender, Washington Mutual – and that’s the only payment he ever made. He has claimed bankruptcy seven times and filed four lawsuits over the years, all focused on letting him stay in the home. (more…)

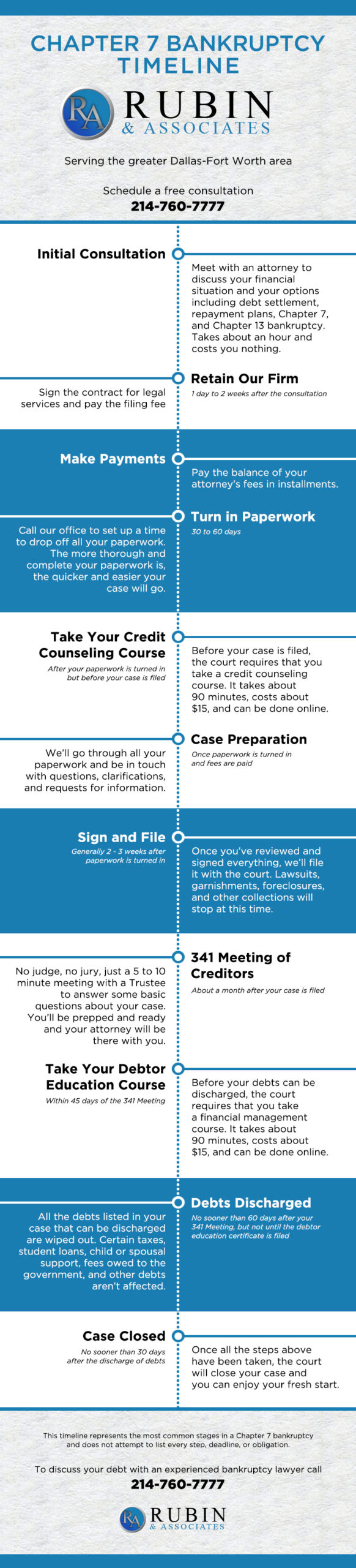

Filing for bankruptcy is a huge decision, and usually it has to be made under pretty extreme stress. Your circumstances are unique – so the best way to know if you should file is to call us at 214-760-7777 for a free consultation. The pandemic and ensuing lockdowns have made the situation even more stressful for many DFW area residents. This post will help answer a few high level questions, but it is always better to talk to an expert to get answers about your specific situation.

Filing for bankruptcy is a huge decision, and usually it has to be made under pretty extreme stress. Your circumstances are unique – so the best way to know if you should file is to call us at 214-760-7777 for a free consultation. The pandemic and ensuing lockdowns have made the situation even more stressful for many DFW area residents. This post will help answer a few high level questions, but it is always better to talk to an expert to get answers about your specific situation. It’s tax season again, and with the COVID tax delay, taxes are almost due. Every spring, we hear lots of questions from potential clients about the tax implications of filing for bankruptcy. It’s a fairly simple answer – it depends on whether the debt was discharged in bankruptcy or just forgiven by the creditor.

It’s tax season again, and with the COVID tax delay, taxes are almost due. Every spring, we hear lots of questions from potential clients about the tax implications of filing for bankruptcy. It’s a fairly simple answer – it depends on whether the debt was discharged in bankruptcy or just forgiven by the creditor. It’s a question we hear all the time – after a client files their bankruptcy case, they ask us “Should I keep my car?”

It’s a question we hear all the time – after a client files their bankruptcy case, they ask us “Should I keep my car?” You have just filed your bankruptcy case, and now you are on pins and needles. You’ve gotten all the paperwork together, answered all our “lawyer questions”, and filed all of your schedules with the court. What happens now?

You have just filed your bankruptcy case, and now you are on pins and needles. You’ve gotten all the paperwork together, answered all our “lawyer questions”, and filed all of your schedules with the court. What happens now?

As most of the country is experiencing the second round of coronavirus-related lockdowns, many Americans are wondering how COVID will affect the already stressed economy. While bankruptcy cases have slowed in recent months, most experts agree that the number of cases filed will rise significantly as we move into 2021.

As most of the country is experiencing the second round of coronavirus-related lockdowns, many Americans are wondering how COVID will affect the already stressed economy. While bankruptcy cases have slowed in recent months, most experts agree that the number of cases filed will rise significantly as we move into 2021. The holiday season is upon us again, with Black Friday and Cyber Monday just a few weeks away. The holiday season, and Black Friday in particular, are designed to get Americans to spend as much money as possible. This year, the COVID lockdowns will change the way people shop for the holidays. The doorbuster shopping events won’t happen this year – everyone will be shopping from home.

The holiday season is upon us again, with Black Friday and Cyber Monday just a few weeks away. The holiday season, and Black Friday in particular, are designed to get Americans to spend as much money as possible. This year, the COVID lockdowns will change the way people shop for the holidays. The doorbuster shopping events won’t happen this year – everyone will be shopping from home.  Many times, financial difficulty leads to stress in a marriage. In cases where the financial stress leads to divorce, the issues often lead to bankruptcy filings.

Many times, financial difficulty leads to stress in a marriage. In cases where the financial stress leads to divorce, the issues often lead to bankruptcy filings.